In his 2009, $787 billion economic recovery stimulus plan, President Obama allocated $263 billion toward subsidizing state and local governments that were experiencing historic tax revenue shortfalls and rising costs directly due to the deep and extended recession. As of March 2011, more than 92 percent of Obama's original $787 billion stimulus has been spent and only $23 billion remains of the $263 billion total allocated to states and cities. With those state and local governments' subsidies essentially used up, Republican and center-right Democratic governors elected last November have turned toward making public employees pay with their jobs, wages, and benefits for the now re-emerging deficits; so too with those least able to afford to pay

In his 2009, $787 billion economic recovery stimulus plan, President Obama allocated $263 billion toward subsidizing state and local governments that were experiencing historic tax revenue shortfalls and rising costs directly due to the deep and extended recession. As of March 2011, more than 92 percent of Obama's original $787 billion stimulus has been spent and only $23 billion remains of the $263 billion total allocated to states and cities. With those state and local governments' subsidies essentially used up, Republican and center-right Democratic governors elected last November have turned toward making public employees pay with their jobs, wages, and benefits for the now re-emerging deficits; so too with those least able to afford to pay

The causes of local budget deficits are first and foremost attributable to the recent recession, the worst since the 1930s. Acknowledging the severity of the recession as the primary cause of the fiscal crisis, the Federal Reserve Board of San Francisco noted in its Economic Letter last year that the resultant collapse of local government tax revenues was "the most severe since at least 1947 when these data began to be collected." In addition to the depth of the recession, the "recovery" has been the weakest on record of any recession in the past 60 years.

The "recovery" has also been the most lopsided. Wealthy investors, bankers, S&P 500 corporations, and the top 10 percent of U.S. households (about 11 million) have all recovered nicely. The stock market has risen 100 percent, the bond markets the past two years have witnessed the greatest boom in half a century, medium and large corporations are sitting on a trove of $2 trillion in cash, and banks are hoarding $1 trillion in excess reserves. Meanwhile, corporations refuse to invest and create jobs with that $2 trillion, while banks refuse to lend to small businesses, with bank lending falling 13 percent in the past year.

For the bottom 90 percent of households (more than 100 million) the picture is decidedly not one of recovery. More than 20 million people are still jobless, home foreclosures approach 10 million, another 12 million mortgages are "under water," and home prices are falling once again.

Though the ultimate cause of state and local governments' fiscal crises at present is therefore grounded in the deep economic contraction of 2008-2009, it is due just as well to the Obama administration's economic recovery strategy—a strategy that ultimately failed to ensure the business investing and job creation which would have restored state and local governments' tax revenues. Obama's great strategic error was to decide to bail out the banks and corporate America at taxpayer expense, in the assumption that once having been "bailed out" they would do their part and follow through with lending, investing, and creating jobs. But that didn't happen. And it left Obama with no Plan B except to go, hat in hand, to corporate America begging them to create jobs—as his recent February speech to the U.S. Chamber of Commerce illustrated.

Additional Causes of Fiscal Crises

Besides the recession and the failure of Obama's stimulus, there are at least four other specific causes of states and city budget deficits. None of these include public workers' wages or benefits.

For three decades the general policy trend across nearly all states has been to reduce taxes on business and investors. For decades, they have been attempting to lure companies from other states by granting handsome tax concessions if they relocate company headquarters and other facilities. It has resulted in a steady drop over the longer term in the corporate share of state total tax revenues. The result has been a tax revenue race to the bottom, depressing state tax revenues over the long run and adding to the weak recovery's short run negative impact. It becomes even worse when we add to this trend the more general trend of granting in-state resident corporations and businesses further tax cuts.

The myth that business tax cuts create jobs is not supported by the evidence. For example, during the Bush years more than $3.4 trillion in tax cuts were passed, 80 percent of which (about $2.7 trillion) went to investors and businesses. It produced the slowest job growth since 1945 following a recession. It took 46 months following the 2001 recession just to recover the level of jobs that existed on the eve of the recession. Another example in the current recession: more than $300 billion in tax cuts were introduced in 2009, resulting in the $2 trillion cash hoard by business noted previously. That $300 billion produced less than 1 million full time equivalent jobs the past 2 years. That tax cut cost the U.S. $300,000 for every job created by corporations to date. Not a very good investment by any measure. Estimates are it will take 7-8 years at best to return to a level of jobs in the U.S. economy that existed in 2007.

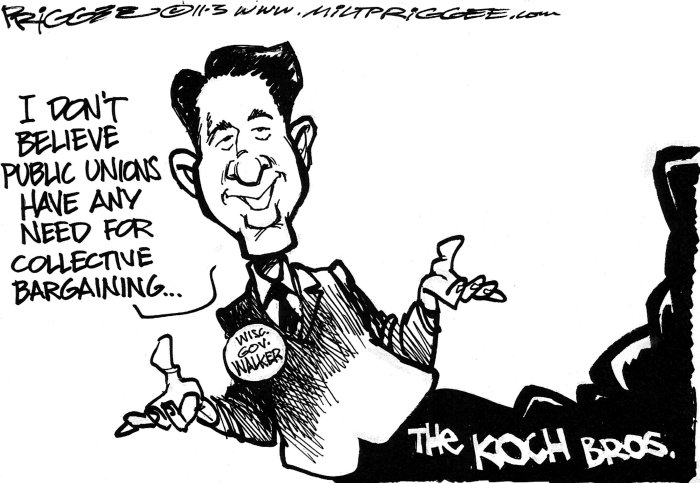

In recent months, Wisconsin Governor Scott Walker, with the encouragement and assistance of the billionaire Koch brothers, launched a direct attack on public workers in Wisconsin. The immediate target was to strip Wisconsin workers of the right to collectively bargain. The ultimate target, however, was to strip them of their jobs, current level of wages, and pension and health-care benefits. Attacking collective bargaining was just the means to the objective of making public workers pay for the deficit.

Less well known to the general public, however, is that the current year's Wisconsin deficit is the result of recent business tax cuts. Walker granted $120 million in tax cuts for businesses in the past year. The state's budget deficit is $137 million. In short, the business tax cuts are what created this year's deficit in Wisconsin, not public workers. But public workers are nonetheless targeted to pay the bill. The story is not much different in many other states.

Another major element of state and city deficits is the return this past year of double digit annual increases in health-care costs. As the U.S. Government Accountability Office recently reported, "the primary driver of fiscal challenges for state and local government continues to be growth in health costs."

Republican governors and the business press distort this fact and make it appear as if the reason for rising health costs is that public workers have been getting big increases in health care benefits for years, thus creating the budget deficits. But rising health-care costs aren't necessarily associated with rising benefits for workers. In fact, benefit coverage levels for public workers—like their private worker counterparts—have been falling as health care insurance premium costs rose at double digit rates between 1997-2007 in the run-up to the recent recession. And as U.S. Department of Labor data for the past year show, total benefit cost increases for state and local government workers amounted to only 0.6 percent. And that's for health care, pensions, and all other benefits.

The far greater impact on budget deficits in this area is from health cost increases associated with Medicaid, not public employee health benefits. Medicaid accounts for more than 20 percent of all state spending, and the return of double-digit annual increases in health care costs has intensified their budget deficit problems.

When debate was launched in 2009 on national health care reform, health insurance companies tempered their cost increases to single digit levels. That lasted barely one year. Once the Obama health care bill was passed in 2010, without the public option and with virtually no containment of health costs in it, health insurance premiums began rising again at double digit levels. In some cases the increases have been 30 and 40 percent. These increases are the product of health insurance companies once again running amuck, not of exorbitant increases in public workers' health benefits.

Yet another area of sharply rising costs for local governments, is the borrowing in the municipal bond market. Since mid-2010, especially, investors have been pulling their money out of the municipal bond market where states and cities borrow heavily to cover their budget deficits. As investors have been pulling out, the cost of borrowing has risen, further exacerbating budget deficits. And as their deficits grow, their borrowing rates rise still further, as do their costs. It has become a vicious circle, with borrowing costs rising, deficits worsening, and investors leaving. Making this situation still worse was the Obama administration's withdrawal of subsidies for the municipal bond markets late in 2010, which had the effect of lowering states' borrowing rates. In short, the longer-term outlook for borrowing costs is negative. Borrowing costs will rise, further exacerbating budget deficits. The municipal bond market promises to weaken in the months to come, raising the specter, as some have been predicting, of a subprime market-like bust in the municipal bond market at some point in the near future.

The collapse of the residential housing market since 2007 has also severely impacted city and county government deficits. The housing collapse has meant a more than 30 percent fall in home prices on average, and up to 50 percent in some localities. That has translated into falling property values and local property taxes, on which local governments depend in particular. The failure of home prices to recover (and in fact now entering a double dip decline) has drawn out the problem of local property tax recovery.

Local governments and school districts also experienced serious long-term budget losses as a consequence of speculating in derivatives. Typically, banks would sell cities and school districts on speculating in risky interest rate swaps, a form of derivatives, which caused most government entities to suffer significant losses.

It's Not Wages

According to the U.S. Labor Department, wages for government workers in 2010 rose only 1.2 percent, lower than the official inflation rate. And that 1.2 percent does not include the reduction in total take home pay for the multiple "furloughs" (days off without pay) initiated throughout the public sector in recent years. Nor does it include lost pay for the millions shifted from full time work to part time work. (Part time wages are not included in the annual wage calculation.) Nor does it include the several hundred thousand who lost their jobs in 2010. When these latter reductions in pay are properly factored in, the total wage gain by public workers last year was almost certainly less than 1 percent. In comparison, private industry wages rose 1.8 percent in 2010.

An argument heard frequently by those attacking public workers is that while their wages may be low, public workers get huge benefit increases, especially pension benefits. But the facts don't support that claim either. The U.S. Labor Department's total compensation for public workers, which includes wages plus benefits, rose only 1.8 percent last year. In other words, all types of benefits combined amounted collectively to only a 0.6 percent increase. In comparison, private sector workers' total compensation rose 2.1 percent. This pattern has been true since the recession began, and even before.

Ignoring the recent record on wages and benefits in the short term, those attacking public workers argue that the longer-term trend shows public worker wages in recent decades have risen above that of their counterparts in the private sector. But there are several problems with this line of argument. First, it ignores the fact that public workers' level of education, in general, is higher than that for the private sector, in general. When education levels are compared, public to private, public workers' wage levels and wage gains the past two decades are not any higher than private sector counterparts.

Second, the destruction of unions in the private sector has been occurring since at least the late 1970s. Over the past three decades the real weekly earnings of the bottom 90 percent of the work force has stagnated, at best, and fallen for most of those below the midpoint. The private unionized workforce was 22 percent in 1980. Today it is less than 7 percent. In contrast, public workers' unions still represent around 35 percent of the public workforce. They have been able to maintain their wage and earnings levels as a result. Up to now, concession bargaining has not been a major characteristic of the public sector, unlike the private sector, where real wages and earnings have stagnated and fallen as a consequence of three decades of concession bargaining. For example, autoworkers make less than half of what they did just a decade ago. So what looks like increases in relative wages for public workers is really a relative decline in the wages and earnings of private sector workers.

It's Not Pension Benefits

An even bigger misrepresentation is associated with public workers' pension benefits as underfunded future pension liabilities are cleverly thrown into states' general operating budgets to make it appear as if the projected budget deficits will rise. The element of public worker pension benefit costs is part smoke and mirrors and part real.

Republican governors leading the charge against public employees, like Chris Christie of New Jersey, estimated this past January 2011 that the pension funding gap for all states combined rose to $2 trillion from 2009. Christie then maintained it reached $2.5 trillion in 2010. If the pension gap doubled from $1 trillion to $2 trillion in 2009, and that year was the year of the banking and financial collapse in the U.S., the shortfall must obviously have to do with the financial collapse of 2008-2009. But to believe Christie, employee pensions were the cause of the doubling of the gap. If that were true, then one might expect that public workers' pension benefits must have doubled to explain the increase in the funding gap. But that's nonsense. As previously noted, the recent total benefits gain for public workers was only 0.6 percent. That could not have caused a $1 trillion rise in the pension funding gap.

Christie's feeble argument aside, there is nevertheless indeed a pension funding gap. Many state and local governments' pensions are underfunded. The Pew Center for the States estimated at the end of fiscal year 2008 that the funding gap for pensions, health care, and other benefits was about $1 trillion. (Note that that gap included more than just pension benefits. About half that, or $500 billion, was underfunded pensions.) Currently, underfunded public pensions are approximately $1 trillion, according to the National Association of State Budget Officers. But the key question is, what are the causes of this underfunding or pension gap? Is it unrestrained increases in public workers' pension benefits? Or is it the product of something else?

In fact, public workers' pension costs are not the result of out of control pension benefit increases, but of pension fund managers' negligence and, arguably, their financially criminal activity.

Public pension fund managers over the last decade consistently speculated fast and loose with risky financial instruments, in partnership with hedge funds and other shadow banks. That risky investing has caused record losses in pension fund balances. Those recent losses, moreover, followed decades of pension fund managers declaring "contribution holidays"—i.e., refusal to make required contributions to the pension funds—that further undermined the health of their pension funds. Speculative investments gone bust and failure to make contributions are the two causes of public pension underfunding. It is this underfunding that governors are manipulating to project a bloated deficit, to be used as a pretext for attacking public workers pensions, health benefits, and wages.

A typical example of this was recently reported by the Wall Street Journal on January 25, 2011. The Illinois state employee pension system is only 50 percent funded, with liabilities of $136 billion as of the end of 2010. However, the cause is not excessive employee pension benefit increases. "The under-funding, one of the worst among states in the nation, is partly the result of the state frequently skipping its recommended contributions to the fund." Unfortunately, the Journal ignored the second element of Illinois' pension fund liability gap: how much of that gap was due to losses on bad investments.

Public employee pension benefits and costs have certainly not doubled in the past two years. In fact, they've hardly risen over the past decade. Take, for example, California, a state with one of the worst budget deficits. Anecdotal horror stories appear almost daily in the press about huge pension payouts for public sector retirees. But the fact is that CalPERS, the state employees pension fund, pays out barely $1,000 a month in retirement benefits to just under half of its current retirees. That's only $12,000 a year—and well below the $19,800 official poverty income level. Another 30 percent receive $3,000 a month or less. And that's pre-tax.

Solutions to Budget Deficits and the Pension Gap

The solutions to state and local government budget deficits must target the true causes of those deficits. Some suggestions include:

· Business refusal to spend its $2 trillion hoard of cash on jobs is the greatest cause of the deficits. The federal government should initiate an appropriate tax on businesses that don't invest and create jobs and use the proceeds from the tax to subsidize local government services and jobs.

· Legislation should be introduced in Congress to prevent business relocations to lower tax states solely for the purpose of lowering taxes. A federal tax equivalent should be paid by all companies that do relocate to a lower tax state for up to a period to three years. The proceeds would be paid to the state losing the company, earmarked for state job creation.

· A ceiling equal to the annual change in the consumer price index should be set for increases in health care premium charges by health insurers to state and local governments. Should the insurers refuse to provide services at that cost, then the federal government should extend its current Congressional employees' health plan to the states, covering all state employees and Medicaid recipients.

· The federal government should reintroduce the Build America Bonds subsidy to states and cities borrowing in the municipal bond market to lower their rates of borrowing costs. A bank tax should be levied on banks, the proceeds of which would be used to finance the muni bond subsidy.

· The Federal Reserve Bank should provide annual loans of $500 billion for the next two years to provide bridge loans to those state and local government pension plans with funding gaps below 85 percent. If the Federal Reserve can loan banks (which caused the financial crisis and much of the pension gap) $9 trillion, and foreign banks $1 trillion of that $9 trillion, then it can lend financial institutions like public workers pension funds at least the same it loaned foreign banks.

· Amend the Pension Act of 2006 to prohibit public worker pension funds from investing in hedge funds and other speculative financial institutions. Pension funds should be prohibited from investing in derivatives of all types.

· Public worker pension funds should place a ceiling on the amount of pension payable to high salaried administrators equal to no more than 125 percent of the highest paid public employee in the system.

· Banks, brokers, and other financial intermediaries should be required to make whole financially those cities and school districts misled into participating in interest rate swaps from 2003 to the 2008 financial collapse.

There are three great crises within the economic downturn preventing the U.S. from achieving a true, sustained recovery: the jobs crisis, where more than 20 million remain unemployed; the homeowners crisis, where foreclosures plague more than 10 million and the housing sector remains mired in a bona fide depression; and the growing fiscal crisis of state and local governments. Without addressing these three crises, there can be no sustained economic recovery. Moreover, the longer they are not addressed, the more likely the current general economic crisis will deteriorate once more, resulting in a more serious downturn of the economy.

Z

Jack Rasmus is the author of Epic Recession: Prelude To Global Depression and the forthcoming Obama's Economy: Recovery For The Few (both from Pluto Press).