We have had [in England], ever since 1876, a chronic state of stagnation in all dominant branches of industry. Neither will the full crash come; nor will the period of longed-for prosperity to which we used to be entitled before and after it. A dull depression, a chronic glut of all markets for all trades, that is what we have been living in for nearly ten years. How is this?

—Frederick Engels1

The Great Financial Crisis and the Great Recession began in the United States in 2007 and quickly spread across the globe, marking what appears to be a turning point in world history. Although this was followed within two years by a recovery phase, the world economy five years after the onset of the crisis is still in the doldrums. The United States, Europe, and Japan, remain caught in a condition of slow growth, high unemployment, and financial instability, with new economic tremors appearing all the time and the effects spreading globally. The one bright spot in the world economy, from a growth standpoint, has been the seemingly unstoppable expansion of a handful of emerging economies, particularly China. Yet, the continuing stability of China is now also in question. Hence, the general consensus among informed economic observers is that the world capitalist economy is facing the threat of long-run economic stagnation (complicated by the prospect of further financial deleveraging), sometimes referred to as the problem of “lost decades.”2 It is this issue of the stagnation of the capitalist economy, even more than that of financial crisis or recession, that has now emerged as the big question worldwide.

Within the United States dramatic examples of the shift in focus from financial crisis to economic stagnation are not difficult to find. Ben Bernanke, chairman of the Federal Reserve Board, began a 2011 speech in Jackson Hole, Wyoming, entitled “The Near- and Longer-Term Prospects for the U.S. Economy,” with the words: “The financial crisis and the subsequent slow recovery have caused some to question whether the United States…might not now be facing a prolonged period of stagnation, regardless of its public policy choices. Might not the very slow pace of economic expansion of the past few years, not only in the United States but also in a number of other advanced economies, morph into something far more long-lasting?” Bernanke responded that he thought such an outcome unlikely if the right actions were taken: “Notwithstanding the severe difficulties we currently face, I do not expect the long-run growth potential of the U.S. economy to be materially affected by the crisis and the recession if—and I stress if—our country takes the necessary steps to secure that outcome.” One would of course have expected such a declaration to be followed by a clear statement as to what those “necessary steps” were. Yet, this was missing from his analysis; his biggest point simply being that the nation needs to get its fiscal house in order.3

Robert E. Hall, then president of the American Economic Association (AEA), provided a different approach in an address to the AEA in January 2011, entitled “The Long Slump.” A “slump,” as Hall defined it, is the period of above-normal unemployment that begins with a sharp contraction of the economy and lasts until normal employment has been restored. The “worst slump in US history,” Hall stated, was “the Great Depression in which the economy contracted from 1929 to 1933 and failed to return to normal until the buildup for World War II.” Hall labeled the period of prolonged slow growth in which the U.S. economy is now trapped “The Great Slump.” With government seemingly unable to provide the economy with the needed stimulus, he observed, there was no visible way out: “The slump may last many years.”4

In June 2010, Paul Krugman wrote that the advanced economies were currently caught in what he termed the “Third Depression” (the first two being the Long Depression following the Panic of 1873 and the Great Depression of the 1930s). The defining characteristic of such depressions was not negative economic growth, as in the trough of the business cycle, but rather protracted slow growth once economic recovery had commenced. In such a long, drawn-out recovery “episodes of improvement were never enough to undo the damage of the initial slump, and were followed by relapses.” In November 2011, Krugman referred to “The Return of Secular Stagnation,” resurrecting the secular stagnation hypothesis of the late 1930s to early ‘50s (although in this case, according to Krugman, the excess savings inducing stagnation are global rather than national).5

Books too have been appearing on the stagnation theme. In 2011, Tyler Cowen published The Great Stagnation, which quickly became a bestseller. For Cowen the U.S. economy has been characterized by a “a multi-decade stagnation…. Even before the financial crisis came along, there was no new net job creation in the last decade…. Around the globe, the populous countries that have been wealthy for some time share one common feature: Their rates of economic growth have slowed down since about 1970.”6 If creeping stagnation has been a problem for the U.S. and other advanced economies for some time, Thomas Palley, in his 2012 book, From Financial Crisis to Stagnation, sees today’s Great Stagnation itself as being set off by the Great Financial Crisis that preceded it, and as representing the failure of neoliberal economic policy.7

Such worries are not confined to the United States, given the sluggish economic growth in Japan and Europe as well. Christine Lagarde, managing director of the IMF, gave a speech in Washington in September 2011 in which she stated that the world economy has “entered a dangerous new phase of the crisis…. Overall, global growth is continuing, but slowing down,” taking the form of an “anemic and bumpy recovery.” Fundamental to this dangerous new phase of crisis was “core instability,” or weaknesses in the Triad—North America, Europe, and Japan—along with continuing financial imbalances “sapping growth.” The big concern was the possibility of another “lost decade” for the world economy as a whole. In November 2011 Lagarde singled out China as a potential weak link in the world economic system, rather than a permanent counter to world economic stagnation.8

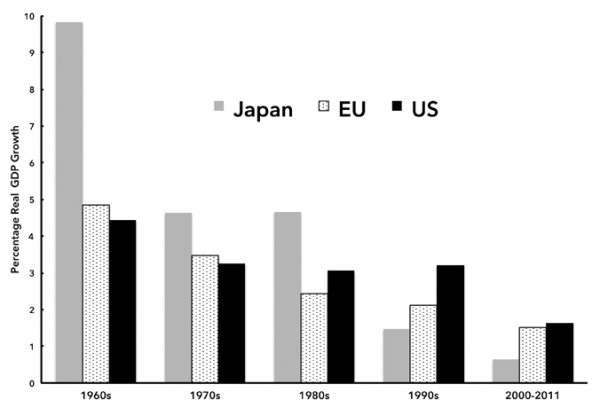

The fact that these rising concerns with respect to the slowing down of the wealthy Triad economies have a real basis, not just in the last two decades but also in long-term trends since the 1960s, can be seen in Chart 1. This shows the declining real growth rates of the Triad economies in the decades from the 1960s to the present. The slowdowns were sharpest in Japan and Europe. But the United States too experienced a huge drop in economic growth after the 1960s, and was unable to regain its earlier trend-rate of growth despite the massive stimuli offered by military-spending increases, financial bubbles, a growing sales effort, and continuing exploitation of the privileged position of the dollar as the hegemonic currency. The bursting of the New Economy stock market bubble in 2000 seriously weakened the U.S. economy, which was only saved from a much larger disaster by the rapid rise of the housing bubble in its place. The bursting of the latter in Great Financial Crisis of 2007–09 brought the underlying conditions of stagnation to the surface.

Hence, long-term economic slowdown, as Chart 1 indicates, preceded the financial crisis. In the U.S case, the rate of growth for the 1970s (which was slightly higher than that of the two subsequent decades) was 27 percent less than in the 1960s. In 2000–2011 the rate of growth was 63 percent below that of the 1960s.9 It was this underlying stagnation tendency, as we shall argue in this book, which was the reason the economy became so dependent on financialization—or a decades-long series of ever-larger speculative financial bubbles.10 In fact, a dangerous feedback loop between stagnation and financial bubbles has now emerged, reflecting the fact that stagnation and financialization are increasingly interdependent phenomena: a problem that we refer to in this book as the stagnation-financialization trap.

The Denial of History

Although the tendency to stagnation or a long period of anemic growth is increasingly recognized even within the economic mainstream as a major issue, broad historical and theoretical understandings of this and its relation to capitalist development are lacking within establishment circles. The reason for this we believe can be traced to the fact that neoclassical economists and mainstream social science generally have long abandoned any meaningful historical analysis. Their abstract models, geared more to legitimizing the system than to understanding its laws of motion, have become increasingly other-worldly—constructed around such unreal assumptions as perfect and pure competition, perfect information, perfect rationality (or rational expectations), and the market efficiency hypothesis. The elegant mathematical models developed on the basis of these rarefied constructions often have more to do with beauty in the sense of ideal perfection, than with the messy world of material reality. The results therefore are about as relevant to today’s reality as the medieval debates on the number of angels that could fit on the end of a pin were to theirs. This is an economics that has gone the way of stark idealism—removed altogether from material conditions. As Krugman put it, “the economics profession went astray because economists, as a group, mistook beauty, clad in impressive-looking mathematics, for truth.”11

John Kenneth Galbraith, in The Economics of Innocent Fraud, provided a still stronger condemnation of prevailing economic and social science, arguing that in recent decades the system itself had been fraudulently “renamed” from capitalism to “the market system.” The advantage of the latter term from an establishment perspective was: “There was no adverse history here, in fact no history at all. It would have been hard, indeed, to find a more meaningless designation—this is a reason for the choice…. So it is of the market system we teach the young…. No individual or firm is thus dominant. No economic power is evoked. There is nothing here from Marx or Engels. There is only the impersonal market, a not wholly innocent fraud.” Along with this, “the phrase ‘monopoly capitalism,’ once in common use,” Galbraith charged, “has been dropped from the academic and political lexicon.” Perhaps worst of all, the growing likelihood of a severe crisis and a long-term slowdown in the economy was systematically hidden from view by this fraudulent displacement of the very idea of capitalism (and even of the corporate system).12

The continuing influence of Galbraith’s “economics of innocent fraud” and the absurd results it generates can be seen in a 2010 speech by Bernanke at Princeton, entitled “Implications of the Financial Crisis for Economics.” The primary reason the “standard [macroeconomic] models” had failed to see the Great Financial Crisis coming, Bernanke admitted, was that these models “were designed for…non-crisis periods” only. In other words, the conventional models employed by orthodox economists were constructed (intentionally or unintentionally) so as toexclude the very possibility of a major crisis or a long-term period of deepening economic stagnation. As long as economic growth appeared robust, Bernanke told his listeners, the models proved “quite useful.” The problem, then, he insisted, was not so much that the models on which economic analysis and policy were based were “irrelevant or at least significantly flawed.” Rather the bursting of the financial bubble and the subsequent crisis represented events that were not supposed to happen, and that the models were never meant to explain.13This is similar to a meteorologist who has constructed a model that predicts perpetual sunny days interrupted by the occasional minor shower and when the big storm comes claims in the model’s defense that it was never intended to account for the possibility of such unlikely and unforeseen events.14

All of this points to the lack within mainstream economics and social science of a reasoned historical interpretation. “Most of the fundamental errors committed in economic analysis,” Joseph S

ZNetwork is funded solely through the generosity of its readers.

Donate