Five years after the Great Financial Crisis of 2007–09 began there is still no sign of a full recovery of the world economy. Consequently, concern has increasingly shifted from financial crisis and recession to slow growth or stagnation, causing some to dub the current era the Great Stagnation.1 Stagnation and financial crisis are now seen as feeding into one another. Thus IMF Managing Director Christine Lagarde declared in a speech in China on November 9, 2011, in which she called for the rebalancing of the Chinese economy:

The global economy has entered a dangerous and uncertain phase. Adverse feedback loops between the real economy and the financial sector have become prominent. And unemployment in the advanced economies remains unacceptably high. If we do not act, and act together, we could enter a downward spiral of uncertainty, financial instability, and a collapse in global demand. Ultimately, we could face a lost decade of low growth and high unemployment.2

To be sure, a few emerging economies have seemingly bucked the general trend, continuing to grow rapidly—most notably China, now the world’s second largest economy after the United States. Yet, as Lagarde warned her Chinese listeners, “Asia is not immune” to the general economic slowdown, “emerging Asia is also vulnerable to developments in the financial sector.” So sharp were the IMF’s warnings, dovetailing with widespread fears of a sharp Chinese economic slowdown, that Lagarde in late November was forced to reassure world business, declaring that stagnation was probably not imminent in China (the Bloomberg.com headline ran: “IMF Sees Chinese Economy Avoiding Stagnation.”)3

Nevertheless, concerns regarding the future of the Chinese economy are now widespread. Few informed economic observers believe that the current Chinese growth trend is sustainable; indeed, many believe that if China does not sharply alter course, it is headed toward a severe crisis. Stephen Roach, non-executive chairman of Morgan Stanley Asia, argues that China’s export-led economy has recently experienced two warning shots: first the decline beginning in the United States following the Great Financial Crisis, and now the continuing problems in Europe. “China’s two largest export markets are in serious trouble and can no longer be counted on as reliable, sustainable sources of external demand.”4

In order to avoid looming disaster, the current economic consensus suggests that the Chinese economy needs to rebalance its shares of net exports, investment, and consumption in GDP—moving away from an economy that is dangerously over-reliant on investment and exports, characterized by an extreme deficiency in consumer demand, and increasingly showing signs of a real estate/financial bubble. But the very idea of such a fundamental rebalancing—on the gigantic scale required—raises the question of contradictions that lie at the center of the whole low-wage accumulation model that has come to characterize contemporary Chinese capitalism, along with its roots in the current urban-rural divide.

Giving life to these abstract realities is the burgeoning public protest in China, now consisting of literally hundreds of thousands of mass incidents a year—threatening to halt or even overturn the entire extreme “market-reform” model.5 China’s reliance on its “floating population” of low-wage internal migrants for most export manufacture is a source of deep fissures in an increasingly polarized society. And connected to these economic and social contradictions—that include huge amounts of land seized from farmers—is a widening ecological rift in China, underscoring the unsustainability of the current path of development.

Nor are China’s contradictions simply internal. The complex system of global supply chains that has made China the world’s factory has also made China increasingly dependent on foreign capital and foreign markets, while making these markets vulnerable to any disruption in the Chinese economy. If a severe Chinese crisis were to occur it would open up an enormous chasm in the capitalist system as a whole. As the New York Times noted in May 2011, “The timing for when China’s growth model will run out of steam is probably the most critical question facing the world economy.”6 More important than the actual timing, however, are the nature and repercussions of such a slowdown.

Capitalist Contradictions with Chinese Characteristics

For many the idea that the Chinese economy is rife with contradictions may come as something as a surprise since the hype on Chinese growth has expanded more rapidly than the Chinese economy itself. As the Wall Street Journal sardonically queried in July 2011, “When exactly will China take over the world? The moment of truth seems to be coming closer by the minute. China will become the largest economy by 2050, according to HSBC. No, its 2040, say analysts at Deutsche Bank. Try 2030, the World Bank tells us. Goldman Sachs points to 2020 as the year of reckoning, and the IMF declared several weeks ago that China’s economy will push past America’s in 2016.” Not to be outdone, Harvard historian Niall Ferguson declared in his 2011 book, Civilization: The West and the Rest, that “if present rates persist China’s economy could surpass America’s in 2014 in terms of domestic purchasing power.”7

This prospect is generally viewed with unease in the old centers of world power. But at the same time the new China trade is an enormous source of profitability for the Triad of the United States, Europe, and Japan. The latest round of rapid growth that has enhanced China’s global role was an essential component of the recovery of global financialized capitalism from the severe crisis of 2007–09, and is counted on in the future.

There are clearly some who fantasize, in today’s desperate conditions, that China can carry the world economy on its back and keep the developed nations from what appears to be a generation of stagnation and intense political struggles over austerity politics.8 The hope here undoubtedly is that China could provide capitalism with a few decades of adequate growth and buy time for the system, similar to what the U.S.-led debt and financial expansion did over the past thirty years. But such an “alignment of the stars” for today’s world capitalist economy, based on the continuation of China’s meteoric growth, is highly unlikely.

“Let’s not get carried away,” the Wall Street Journal cautions us. “There’s a good deal of turmoil simmering beneath the surface of China’s miracle.” The contradictions it points to include mass protests (rising to as many as 280,000 in 2010), overinvestment, idle capacity, weak consumption, financial bubbles, higher prices for raw materials, rising food prices, increasing wages, long-term decline in labor surpluses, and massive environmental destruction. It concludes, “If nothing else, the colossal challenges that lie ahead for China provide an abundance of good reasons to doubt long-term projections of the country’s economic supremacy and global dominance.” The immediate future of China is therefore uncertain, throwing added uncertainty on the entire global economy. As we shall see, not only might Chinanot bail out global capitalism at present, an argument can be made that it constitutes the single weakest link for the global capitalist chain.9

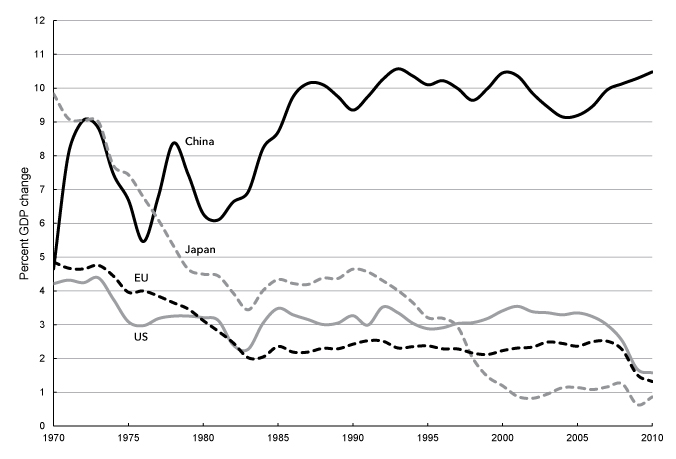

At question is the extraordinary rate of Chinese expansion, especially when compared with the economies of the Triad. The great divergence in growth rates between China and the Triad can be seen in Chart 1 (below), showing ten-year moving averages of annual real GDP growth for the United States, the European Union, and Japan, from 1970 to 2010. While the rich economies of the United States, Western Europe, and Japan have been increasingly prone to stagnation—overcoming this in 1980–2006 only by means of a series of financial bubbles—China’s economy over the same period (beginning in the Mao era) has continually soared. China managed to come out of the Great Financial Crisis period largely unaffected with a double-digit rate of growth, at the same time that what The Economist has dubbed “the moribund rich world” was laboring to achieve any positive growth at all.10

Chart 1. Change in Real GDP, 1970–2010 (Ten-Year Moving Average of Percent Change From Previous Year)

Sources: WDI database for China, Japan, and the European Union (http://databank.worldbank.org) and St. Louis Federal Reserve Database (FRED) for the United States (http://research.stlouisfed.org/fred2/).

To give a sense of the difference that the divergence in growth rates shown in Chart 1 makes with respect to exponential growth, an economy growing at a rate of 10 percent will double in size every seven years or so, while an economy growing at 2 percent will take thirty-six years to double in size, and an economy growing at 1 percent will take seventy-two years.11

The economic slowdown in the developed, capital-rich economies is long-standing, associated with deepening problems of surplus capital absorption or overaccumulation. As the New York Times states, “Mature countries like the United States and Germany are lucky to grow about 3 percent annually”—indeed, today we might say lucky to grow at 2 percent. Japan’s growth rate has averaged less than 1 percent over the period 1992 to 2010. As Lagarde noted in a speech in September 2011, according to the latest IMF projections, “the advanced economies will only manage an anemic 1 1/2-2 percent” growth rate over the years 2011–12. China, in contrast, has been growing at 10 percent.12

The problems of the mature economies are complicated today by two further features: (1) the heavy reliance on financialization to lift the economy out of stagnation, but with the consequence that the financial bubbles eventually burst, and (2) the shift towards the corporate outsourcing of production to the global South. World economic growth in recent decades has gravitated to a handful of emerging economies of the periphery; even as the lion’s share of the profits derived from global production are concentrated within the capitalist core, where they worsen problems of maturity and stagnation in the capital-rich economies.13

As the structural crisis within the center of the capitalist world economy has deepened, the hope has been raised by some that China will serve to counterbalance the tendency toward stagnation at the global level. However, even as this hope has been raised it has been quickly dashed—as it has become increasingly apparent that cumulative contradictions are closing in on China’s current model, producing growing panic within world business.

Ironically, today’s fears regarding the Chinese economy stem in part from the way China engineered its way out of the global slump brought on by the Great Financial Crisis—a feat that was regarded initially by some as conclusive proof that China had “decoupled” itself from the West’s fate and represented an unstoppable growth machine. Faced with the world crisis and declining foreign trade, the Chinese government introduced a massive $585 billion stimulus plan in November 2008, and urged state banks aggressively to make new loans. Local governments in particular ran up huge debts associated with urban expansion and real estate speculation. As a result, the Chinese economy rebounded almost instantly from the crisis (in a V-shaped turnaround). The growth rate was 7.1 percent in the first half of 2009 with state-directed investments estimated as accounting for 6.2 percentage points of that growth.14 The means of accomplishing this was an extraordinary increase in fixed investment, which served to fill the gap left by falling exports.

This can be seen in Table 1, which shows the percent contribution to China’s GDP of consumption, investment, government, and trade (net exports). The sharp increase in investment as a share of GDP, which rose 7 percentage points between 2007–10, mirrored the sharp decrease in the share of both trade and consumption over the same period, which dropped 5 and 2 percentage points, respectively. Meanwhile, the share of government spending in GDP remained steady. Investment alone now constitutes 46 percent of GDP, while investment plus trade equals 52 percent.

Table 1. Percent Contribution to China’s GDP, 2002–2010

|

A |

B |

C |

D |

B+D |

|

|

Consumption |

Investment |

Government |

Trade |

Investment |

|

|

2002 |

44.0 |

36.2 |

15.6 |

4.2 |

40.4 |

|

2003 |

42.2 |

39.1 |

14.7 |

4.0 |

43.1 |

|

2004 |

40.6 |

40.5 |

13.9 |

5.1 |

45.6 |

|

2005 |

38.8 |

39.7 |

14.1 |

7.4 |

47.1 |

|

2006 |

36.9 |

39.6 |

13.7 |

9.7 |

49.3 |

|

2007 |

36.0 |

39.1 |

13.5 |

11.4 |

50.5 |

|

2008 |

35.1 |

40.7 |

13.3 |

10.9 |

51.6 |

|

2009 |

35.0 |

45.2 |

12.8 |

7.0 |

52.2 |

|

2010 |

33.8 |

46.2 |

13.6 |

6.4 |

52.6 |

Sources: Pettis, “Lower Interest Rates, Higher Savings?” http://mpettis.com, October 16, 2011;China Statistical Yearbook.

As Michael Pettis, a professor at Peking University’s Guanghua School of Management and a specialist in Chinese financial markets, explained, the sharp drop in the trade surplus in the crisis might “have forced GDP growth rates to nearly zero.” However, “the sudden and violent expansion in investment” served as “the counterbalance to keep growth rates high.” Of course behind the dramatic ascent of the investment share of GDP, rising 10 percentage points during the years 2002–10, lay the no less dramatic descent of the consumption share, which dropped 10 perentage points over the same period, from 44 percent to 34 percent, the smallest share of any large economy.15

With investment spending running at close to 50 percent in this period the Chinese economy is facing wi

ZNetwork is funded solely through the generosity of its readers.

Donate