This is the second part of a series by Jack Rasmus on the historical context and current trajectory of the financial crisis. The first article appeared in Z Magazine’s February 2010 issue. The second article appeared in Z Magazine’s March 2010 issue.

A year ago the Obama administration assured the nation its $787 billion economic stimulus bill, and three-part bank bailout plan would generate an economic recovery from the current economic crisis. My prediction at the time (Z Magazine, February and March 2009) was that it would fail to generate any sustained economic recovery. The stimulus was not large enough for the U.S. economy, and its composition focused too heavily on business tax cuts, too little on immediate job creation, and did virtually nothing to stop home foreclosures. In addition, the bank bailout program would prove equally unsuccessful, failing to jumpstart bank lending in the U.S.

A year ago the Obama administration assured the nation its $787 billion economic stimulus bill, and three-part bank bailout plan would generate an economic recovery from the current economic crisis. My prediction at the time (Z Magazine, February and March 2009) was that it would fail to generate any sustained economic recovery. The stimulus was not large enough for the U.S. economy, and its composition focused too heavily on business tax cuts, too little on immediate job creation, and did virtually nothing to stop home foreclosures. In addition, the bank bailout program would prove equally unsuccessful, failing to jumpstart bank lending in the U.S.

While U.S. Gross Domestic Product (GDP) turned positive in the second half of 2009, it is still almost certain that there will be a slowdown in GDP growth in the first quarter of 2010. The $787 billion stimulus had only minimal impact in 2009 on the economy and that will begin to fade by mid-year 2010.

What produced the extremely modest, hesitant recovery in the second half of 2009 had more to do with special programs like the first time homebuyers subsidy and cash for clunkers added mid-year, and with technicalities involving inventory adjustments to GDP plus some manufacturing growth tied to U.S. exports growth and more robust recoveries occurring in China and elsewhere. But the cash for clunkers program has been discontinued, resulting at year end 2009 in auto sales immediately retrenching once again. And despite the first time homebuyer program’s extension by Congress, new home sales once again retreated in early 2010. And it too is scheduled to soon expire. To make matters worse, the inventory technicalities are no longer a major factor adding to GDP growth and China and Asia, once absorbing U.S. exports, have begun to tighten spending. So the export push in manufacturing is now fading. The result is that in February the Index of U.S. Manufacturing in the U.S. once more reversed, falling from 58.4 to 56.5 (50.0 represents no growth).

More than 2.5 million manufacturing jobs have been lost in 2008-2009, hardly representing a recovery. Nor can one assume other major sectors of the economy have recovered. The construction industry declined by $200 billion in 2009 and shows no sign of turnaround with new home sales and home prices falling once again. And the far more important Services Industry Index, nearly ten times the size of manufacturing in terms of jobs (95 million vs. 11.5 million), has either continued to fall or remained flat throughout the past year despite the stimulus, the tax cuts, and the Federal Reserve pumping trillions into the banks.

Finally, and most recently, in the last week of February, there appeared a renewed decline in consumer confidence, a rise once again in new jobless claims to 500,000 a month, (now 15 percent higher over last quarter), and the continuing surge in foreclosures (soon to surpass 7 million) with 20 percent-plus in mortgages in negative equity (predicted to reach 10 million). Reflecting the new reality, even the stock market peaked on January 19, 2010 and has remained flat to falling since. In short, it all adds up to a scenario representing anything but a sustained economic recovery.

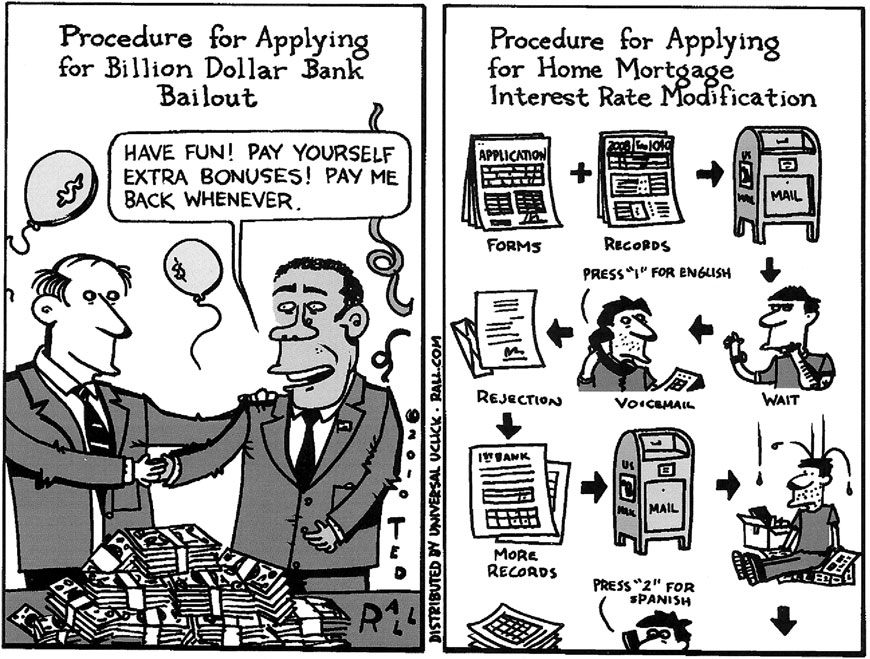

Profits of some of the big 19 banks have indeed risen, but not due to the Obama administration’s early 2009 three-part bailout program. The Obama administration maintained the bailout and finance programs (PIPP, TALF, and HAMP) were necessary to get bank credit flowing again. But lending declined every month throughout 2009. Banks instead borrowed funds from the Federal Reserve at zero percent interest rates and loaned to hedge funds and others at double digit rates to speculate in foreign currency, offshore properties, commodities, and stock markets—or else they speculated directly in their own stocks or bet on foreign government bonds collapsing, as in the case of Greece and elsewhere. On the other hand, essentially nothing has been done to aid the 8,000 small and regional banks, which are now failing by the hundreds, with another 702 on the FDIC’s danger list.

A year later it is now abundantly clear that the Obama administration’s programs were never intended to generate an economic recovery. These programs—the original stimulus, the bank bailout programs, and special one-time programs—all were designed to simply put a floor under the escalating economic collapse at the time. That is quite different than the government generating a true, sustained economic recovery. Putting a temporary floor under the collapse means the Obama strategy was designed simply to buy time to allow a market driven recovery to take hold, to be led by the banks renewing lending once again. But the banks didn’t lend, market forces have been unable to generate a sustained recovery, and except for the big banks, big multinational companies, and the stock markets, the U.S. economy has been simply moving sideways—neither collapsing further nor able to enter a sustained recovery.

It appears the Obama administration’s strategy will continue into 2010. A paltry $15 billion so-called jobs bill, a good part of which is more business tax cuts that will have little effect, is mere tokenism at best. A similar criticism is appropriate for the recent Reid bill (introduced by Democratic Senate leader Harry Reid) providing a mere $1.5 billion for foreclosure aid to five states. Moving through Congress is the more generous $145 billion to continue unemployment benefits and medical insurance subsidies for 6 million workers whose benefits and coverage expires in March. One can support this latter legislation, but it will do nothing to generate jobs or a sustained recovery.

Theory and History

As Part 1 of this series noted, the current crisis is driven by a set of unique characteristics quite different from normal recessions that have occurred in the post-1945 period in the U.S. Unfortunately, Obama administration policymakers have yet to understand this, or else they do and refuse to acknowledge the differences. They have approached the crisis as if it were a normal recession, perhaps somewhat worse in its dimensions, but normal nonetheless. That explains at least in part why the current Administration’s policies have failed to generate a sustained economic recovery. They are essentially policies appropriate for normal recessions, but not for what I call an epic recession.

|

Epic Recessions are the consequence of major financial system implosions. In theoretical terms, those financial busts are the consequence of prior speculative investing excesses, which drive debt and asset price inflation to dangerous levels. When the bust occurs, it produces greater than normal debt unwinding that leads to deflation and defaults. During the boom, speculative phase, the financial system becomes more fragile (i.e., sensitive to implosion) while the rest of the real economy becomes correspondingly more consumption fragile. Both forms of fragility—financial and consumption—fracture when the bust occurs, in turn exacerbating the debt-deflation-default processes that drive the economy in a downward spiral.

However, the most fundamental forces are the consequence of escalating global income inequality, exploding global liquidity with an expanding global money parade of speculators, their new shadow financial institutions, and new markets and financial instruments created for those markets (most notably derivatives). The global money parade, with more than $20 trillion on hand, drives the speculative boom, in the process creating a mountain of debt in the system. Following the bust, only part of the debt is unwound. Much of it remains, obstructing a return to normal lending, investing, and household consumption. Policies designed for normal recessions do not address that mountain of debt overhang, and that is primarily the reason for their relative ineffectiveness in generating a sustained recovery.

To allow the logjam of debt to be slowly worked off only results in an extended period of relative economic stagnation, not sustained recovery. To simply transfer it from banks and businesses to the public balance sheet (U.S. deficit and debt) does nothing to remove it, but only shifts the crisis to the public sector. Putting a floor under the toxic economic waste may prevent a meltdown of the economy’s foundation and core, at least for a while, but does not remove the poisonous material from the economic building. The debt load work off, in other words, must be accelerated and expunged, not simply shifted or transferred. That cannot be achieved piecemeal and incrementally. It must be done with major structural reforms, not normal fiscal-monetary policies.

What is called for is a fundamental restructuring of the financial and tax systems, of income distribution by various measures, a refocusing of spending in a major way on job creation and foreclosure prevention, and addresses the problem of the global money parade of professional speculators, individual and institutional alike.

The following is a brief summary of the major points of an alternative program (detailed more fully in my forthcoming book).

Job Creation & Housing Stabilization

There can be no sustained recovery so long as jobless numbers remain in excess of 20 million (today roughly at 22-23 million when properly calculated) and so long as housing foreclosures, defaults and delinquencies continue to rise, and prices and equity net worth continue to fall. Housing is a problem not simply because of foreclosures, etc., but because of major consumption fragility, or excess debt, that is a major logjam to the return of consumption levels, a sector constituting more than 70 percent of all economic activity. Consumption fragility is a function of both excess debt and insufficient income. Housing is the debt issue; jobs are the income side of the problem. Both must be resolved simultaneously. The Obama administration has sidestepped both. The proposals that follow treat the jobs-housing problem as a consumption fragility problem.

* Reset mortgage rates and mortgage principle to 2002-2007 levels

All loans issued between 2002-07 are included in this provision, not just those facing foreclosure or default. Resetting all loans, not just those at risk of default and foreclosure, is designed not only to reduce excess housing supply coming on the market and driving down housing prices and causing further financial institution write downs and losses, but to serve as a general economy-wide consumption enhancing measure as well. Boosting consumption in this manner provides a continued, long-term consumption effect—unlike one-time government spending stimulus which, once spent, has no further effect. This measure also has the further effect of avoiding the necessity of additional deficit creation. If it affected just 25 million of the 55 million residential mortgages outstanding and reduced mortgage rates by 2 percent on average, the result is more than $200 billion in ongoing consumption every year. The resets may also extend to small business property mortgages, where small business is defined as businesses with less than 50 employees and less than $1 million in annual net income.

* Create new federal agency, HSBLC (Federal Homeowner-business Loan Corporation), to administer nationalized residential mortgage and small business property markets

The HSBLC would provide direct lending to homeowners and small businesses. The initial task of the HSBLC would be to purchase existing mortgages in foreclosure, resetting rates and principal according to the aforementioned formulas. Thereafter, it would extend mortgage financing to all potential home financing in the future. The HSBLC would be the primary agency administering nationalized residential mortgage and small business property markets. The HSBLC would compensate current mortgage lenders not willing to participate in the interest rate and principal resets at a rate of 25 percent of their loan balance in the first year of the resets, and another 25 percent amortized over the remaining 30 years of the reset loans.

* 15 percent homeowners tax credit

All homeowners with mortgages, and those having paid their mortgages in full, are eligible for a 15 percent homeowners investment tax credit on their annual tax returns. The credit would cover investment in items and categories such as home repair, home upgrades, expansion, and major maintenance and improvements, as well as purchases of home consumer appliances like refrigerators, ovens, washer-dryers, etc. The purpose of the provision is to allow homeowners not participating in the resets, the HSBLC mortgage purchases, or new issues to benefit from housing-related consumption measures.

* Moratorium on residential foreclosures and small business property and industrial business loans

A one-year moratorium on residential and small business property foreclosures is proposed in order to prevent further consumption collapse from 4-5 million new foreclosures. The moratorium will apply to small businesses facing Chapter 7 default, suspending default on C&I (commercial and industrial) business loans incurred between 2002-2007 as well.

* $800 billion for job creation and retention

An effective alternative jobs program must carefully consider the composition of employment generation. The quickest way to retain and grow jobs is within existing industries and businesses, not primarily by creating new industries from scratch. Alternative industry infrastructure and energy jobs are part of the program but not its primary focus, due to long delays in job creation for new emerging technologies and industries. A quick path to jobs creation is direct hiring by government, in particular state and local government and school districts. A fast path is promoting hiring in those industries having shown in the past high job growth rates, such as health care. The alternative job creation-retention program also targets jobs in the $50K-$60K annual range on average, with workers receiving a pay level of $40K and benefits load of $10K. Proof of new hiring must precede government payments. The job creation and retention program targets $300 billion for infrastructure jobs, $300 billion for public sector jobs, $100 billion for growth sector jobs like health care, and $100 billion for relocating manufacturing jobs back to the U.S.

An effective alternative jobs program must carefully consider the composition of employment generation. The quickest way to retain and grow jobs is within existing industries and businesses, not primarily by creating new industries from scratch. Alternative industry infrastructure and energy jobs are part of the program but not its primary focus, due to long delays in job creation for new emerging technologies and industries. A quick path to jobs creation is direct hiring by government, in particular state and local government and school districts. A fast path is promoting hiring in those industries having shown in the past high job growth rates, such as health care. The alternative job creation-retention program also targets jobs in the $50K-$60K annual range on average, with workers receiving a pay level of $40K and benefits load of $10K. Proof of new hiring must precede government payments. The job creation and retention program targets $300 billion for infrastructure jobs, $300 billion for public sector jobs, $100 billion for growth sector jobs like health care, and $100 billion for relocating manufacturing jobs back to the U.S.

* $200 billion for social safety net (unemployment insurance, medical coverage, food stamps), trade job loss assistance, and job retraining

Unemployment benefits coverage for one year costs approximately $125 billion, with another $75 billion for full coverage for medical, food stamps, and job retraining assistance.

Tax Restructuring and Program Financing

Three-decades of growing income inequality in the U.S. have provided an important basis for the diversion of trillions of dollars by wealthy investors and corporations to the 27 offshore tax havens, mostly island nations, which the IRS refers to as special jurisdictions. A conservative estimate in 2005 by the investment bank Morgan Stanley found that total holdings in offshore shelters had risen from $250 billion in the mid-1980s to $6 trillion by 2005. Other more recent estimates place the amount up to $11 trillion. With U.S. investors’ and corporations’ share of total world assets estimated at approximately $47 trillion out of a world total of $140 trillion in 2006, according to the business consulting firm McKinsey & Co., it may be safely assumed that U.S. investors share of the $11 trillion held in the 27 offshore tax havens is likely around 34 percent. That translates into roughly $3.74 trillion at minimum.

* U.S. investors must repatriate at least half their offshore shelter assets

This proposal means investors must withdraw and redeposit the $1.87 trillion in U.S. financial institutions located in the U.S. Assuming a long-run return on assets when repatriated to the U.S. of around 15 percent, the $1.87 trillion should yield annual revenues of around $280 billion, which thereafter would be taxed, per this proposal, at the new capital gains rate of 50 percent and yield the U.S. Treasury roughly $140 billion a year in new revenue.

* Foreign profits tax recovery

In 2004 the estimated amount of shielded corporate funds in this area amounted to as much as $700 billion. Offshore corporate retained earnings are likely now in excess of $1 trillion. The return of those earnings reinvested in the U.S. economy would yield a tax revenue stream of at least $100 billion a year.

* Capital incomes tax cuts rollbacks

There are approximately 114 million taxpaying households in the U.S. The wealthiest 1 percent, or 1.1 million, have increased their share of IRS reported income from 8 percent in 1978 to more than 24 percent in 2007. This 24 percent share is equivalent to that which existed for the wealthiest 1 percent in 1928. No long-term recovery is therefore possible without a basic restructuring of the tax system in the U.S., starting with capital incomes taxation. This proposal rolls back tax cuts on capital incomes—i.e., capital gains, dividends, interest and rental incomes for business—to 1981 levels, not 1993. That is, back to that point at which the major tax restructuring began in the U.S. on behalf of earners of capital incomes at the expense of earners of wage incomes.

* Excess speculative profits surtax

This proposal provides for a 70 percent excess profits surtax on returns from speculative investments that exceed a reasonable long-run average (10-15 percent). The tax would extend to contracts on all forms of derivatives, including credit default swaps and other second and third generation financial derivatives products.

* Financial transactions tax

This means financial transactions covering traditional financial assets—such as sales of stocks and bonds, commodities, as well as all securitized asset sales and other forms of financial derivatives assets. This proposal is for a 10 percent tax on all such financial transactions. (The excess speculative profits tax is an additional measure that applies thereafter to profits that may exceed a defined threshold limit, apart from the 10 percent financial transactions tax).

* Retroactive windfall taxes

|

This proposal re-captures taxes the oil-energy companies should have paid on earnings above the companies’ preceding ten year average. This retroactive windfall provision also applies to other companies that reaped rentier profits during the period since 2001. These would include, at minimum, dominant companies in industries like banking, insurance, and pharmaceuticals.

The retroactive windfall tax provision extends, in addition, to excess compensation received by individuals in these companies and industries, in particular CEOs and their senior management teams who have typically received excess compensation as a consequence of their companies’ excess rentier profits position.

* Value-added tax on intermediate goods

Intermediate goods are products and services sold by companies to companies before the final product is sold at retail to consumers. The proposal is therefore not a tax on final, retail sales. The entire proceeds from the tax are allocated to provide financing for a national 401k retirement pool. The level of the VAT on intermediate goods would vary by industry, as well as with the funding requirements of the national 401k retirement pool. An initial tax level of 2 percent is proposed.

* Payroll tax on incomes of wealthiest 1 percent households

With the collapse of defined benefit pension plans and the total failure of private 401k pensions to adequately provide for retirement, more than 70 million retirees in the next decade will experience inadequate levels of income to sustain a reasonable standard of living. That condition will severely exacerbate consumption fragility within the general economy, already in a dire state. Social Security must not only be stabilized but expanded. Thus, this proposal provides extending the current payroll tax rate for Social Security from earned incomes with a ceiling of $107,000 today by adding a new provision that taxes all capital incomes of the wealthiest 1 percent households (with threshold earnings of $332,000 and above) at the current payroll tax rate.

* 10 percent penalty tariffs and non-compliance fees

This proposal includes penalty provisions as disincentives to resistance and non-compliance. For example, corporations that refuse to return foreign profits income to the U.S. for taxation will be levied a 10 percent tariff on all their goods sold in the U.S. until compliance occurs. Similarly, wealthy investors who refuse to repatriate their offshored sheltered earnings will have an unreimbursable 10 percent penalty levied on their remaining earnings or property in the U.S. for the first 90 days of noncompliance. The penalty fee may be increased further with continued non-compliance.

Long-Term Income Restructuring & Consumption Fragility

There can be no long-term solution to the health-care crisis in the U.S. (measured as deteriorating coverage, rising costs, and declining quality of care for the majority) so long as the insurance companies remain a primary player in the system.

* An interim single payer system

As a step toward a Universal Single Payer system, this proposal creates an interim single payer system for the 91 million households earning less than $160,000 per year. Households earning above $160,000 (households within the top 20 percent income distribution) would be exempt, but could participate for a fee that would scale up with their income level.

* National 401k pool

This proposal requires the U.S. government to nationalize the employer-provided and managed 401k plan system and create a single national 401k pool. Each participant would be able to make individual deposits to the pool and withdraw limited amounts from it annually, just as under present employer-managed 401ks. Each account within the pool would be 100 percent portable and immediately vested. Voluntary deposits by individuals into the pool in their own name would be matched by equivalent government contributions. Government matching contributions to the pool would be funded by means of the introduction of a 2 percent national value added tax on the sale of intermediate goods (i.e., a business-to-business sales tax) that all businesses with annual sales revenues of more than $1 million would be required to make. Government investing of the pooled funds would be restricted to public ownership-public works projects or government loans to publicly beneficial joint government-business projects such as alternative energy, green technology, and the like.

* De-privatizing the student loan market

The student loan market returns to a completely de-privatized program where it will function according to its original objective of providing financing to students at cost, in the form of either grants or subsidized loans.

* Re-unionization of the private sector workforce

A long-term program for restoring income to the bottom 80 percent includes policies and measures to restore the unionization rate to at least the 22 percent level of 1980. The first step toward re-unionization must include reforms to level the playing field between workers, their unions, and management regarding legal rights. This begins with implementation of the Employee Free Choice Act (EFCA), which permits a fairer process for union organizing.

* Low and contingent wage indexation

Contingent workers include those who are part time, especially involuntary part time, and the escalating numbers of workers transferred to various kinds of temporary work status. Contingent workers receive, on average, only 70 percent of wages of permanent employed and 10 percent of benefits. Part-time workers mostly receive no benefits and typically half-time pay. These groups’ numbers have risen close to 50 million, approaching one-third of the workforce. The alternative program proposes the minimum wage be adjusted annually according to changes in inflation, much like social security payments to the retired are adjusted annually. This proposal for the first time also introduces a legislated minimum for wages and benefit levels for contingent labor.

Banking System Restructuring & Financial Fragility

Consumer credit markets are too critical and necessary for the functioning of the consumption side of the economy to allow these markets to remain exposed to speculative investing. The following series of proposals provides for restructuring the financial and banking system, focusing on three areas of the financial system that require major changes: the consumer credit markets, the Federal Reserve, and the global money parade of speculators that have been increasingly, and repeatedly, destabilizing the economic system in recent decades.

* Nationalization of consumer credit markets

Residential mortgage, small business property mortgages, and student and auto loans markets should be nationalized, walled off from speculative and profit-seeking banking activity and administered through a new structure of utility banking. A new kind of Federal Reserve system should provide necessary liquidity directly to consumer credit markets, with the credit disbursed by a new network of local credit institutions administered through local government, regulated credit unions, or other non-profit institutional networks.

* Democratize the Federal Reserve

It is necessary to take critical consumer credit markets outside the private, for-profit, sometimes regulated, banking system and run it based on a new concept of utility banking conducted at cost on behalf of consumers and not for profit on behalf of private financial institutions. Providing cost-only loans through the Federal Reserve, functioning as a lender of primary resort, the Fed could be restructured in a new way that democratizes how it operates. Two-thirds of Fed Board of Governors would be elected at large by popular vote. Other proposals would further democratize the Fed and all Federal Reserve deliberations would be public record within 24 hours of meeting.

* Utility banking vs. casino banking

There is a fundamental contradiction between the two principles of banking—banking as a utility and as a speculative profits center. The utility sector includes the now nationalized (according to my earlier proposals) residential mortgage and small business property mortgage markets and consumer credit markets, especially for autos, student loans, and installment credit for big ticket consumer durables products. Utility banking means credit extended at cost and without a profit mark up in the key consumer credit markets. It means the creation of a new network of local financial institutions that take household deposits and issue interest payments equivalent to no more than the cost of credit. New local financial institutions in this system function on a non-profit basis. Their purpose is to provide the essential service of credit provisioning for consumer markets. They may be local government based, non-government local non-profits, or community credit-union like financial institutions.

There is a fundamental contradiction between the two principles of banking—banking as a utility and as a speculative profits center. The utility sector includes the now nationalized (according to my earlier proposals) residential mortgage and small business property mortgage markets and consumer credit markets, especially for autos, student loans, and installment credit for big ticket consumer durables products. Utility banking means credit extended at cost and without a profit mark up in the key consumer credit markets. It means the creation of a new network of local financial institutions that take household deposits and issue interest payments equivalent to no more than the cost of credit. New local financial institutions in this system function on a non-profit basis. Their purpose is to provide the essential service of credit provisioning for consumer markets. They may be local government based, non-government local non-profits, or community credit-union like financial institutions.

* Tame the global money parade

To effectively tame the global money parade requires getting control over its sources of money capital creation as well as its multiple, multi-directional flows. Until the global money parade is routed at minimum from its secretive tax haven dens; until capital flows are taxed, monitored, regulated, and controlled; and until the ever-rising edifice of speculation is prohibited in what is a still growing house of cards derivatives system—the financial instability and fragility in the global system will continue to increase. These proposals raise talking points for a debate on how to address the continuing epic recession and, perhaps, reduce its likelihood of transitioning to a consequent classic global depression in the coming two to five years.