Capital in the Twenty-First Century, by Thomas Piketty, translated from the French by Arthur Goldhammer

Belknap Press/Harvard University Press, 685 pp., $39.95

Thomas Piketty, professor at the Paris School of Economics, isn’t a household name, although that may change with the English-language publication of his magnificent, sweeping meditation on inequality, Capital in the Twenty-First Century. Yet his influence runs deep. It has become a commonplace to say that we are living in a second Gilded Age—or, as Piketty likes to put it, a second Belle Époque—defined by the incredible rise of the “one percent.” But it has only become a commonplace thanks to Piketty’s work. In particular, he and a few colleagues (notably Anthony Atkinson at Oxford and Emmanuel Saez at Berkeley) have pioneered statistical techniques that make it possible to track the concentration of income and wealth deep into the past—back to the early twentieth century for America and Britain, and all the way to the late eighteenth century for France.

The result has been a revolution in our understanding of long-term trends in inequality. Before this revolution, most discussions of economic disparity more or less ignored the very rich. Some economists (not to mention politicians) tried to shout down any mention of inequality at all: “Of the tendencies that are harmful to sound economics, the most seductive, and in my opinion the most poisonous, is to focus on questions of distribution,” declared Robert Lucas Jr. of the University of Chicago, the most influential macroeconomist of his generation, in 2004. But even those willing to discuss inequality generally focused on the gap between the poor or the working class and the merely well-off, not the truly rich—on college graduates whose wage gains outpaced those of less-educated workers, or on the comparative good fortune of the top fifth of the population compared with the bottom four fifths, not on the rapidly rising incomes of executives and bankers.

It therefore came as a revelation when Piketty and his colleagues showed that incomes of the now famous “one percent,” and of even narrower groups, are actually the big story in rising inequality. And this discovery came with a second revelation: talk of a second Gilded Age, which might have seemed like hyperbole, was nothing of the kind. In America in particular the share of national income going to the top one percent has followed a great U-shaped arc. Before World War I the one percent received around a fifth of total income in both Britain and the United States. By 1950 that share had been cut by more than half. But since 1980 the one percent has seen its income share surge again—and in the United States it’s back to what it was a century ago.

Still, today’s economic elite is very different from that of the nineteenth century, isn’t it? Back then, great wealth tended to be inherited; aren’t today’s economic elite people who earned their position? Well, Piketty tells us that this isn’t as true as you think, and that in any case this state of affairs may prove no more durable than the middle-class society that flourished for a generation after World War II. The big idea of Capital in the Twenty-First Century is that we haven’t just gone back to nineteenth-century levels of income inequality, we’re also on a path back to “patrimonial capitalism,” in which the commanding heights of the economy are controlled not by talented individuals but by family dynasties.

It’s a remarkable claim—and precisely because it’s so remarkable, it needs to be examined carefully and critically. Before I get into that, however, let me say right away that Piketty has written a truly superb book. It’s a work that melds grand historical sweep—when was the last time you heard an economist invoke Jane Austen and Balzac?—with painstaking data analysis. And even though Piketty mocks the economics profession for its “childish passion for mathematics,” underlying his discussion is a tour de force of economic modeling, an approach that integrates the analysis of economic growth with that of the distribution of income and wealth. This is a book that will change both the way we think about society and the way we do economics.

1.

What do we know about economic inequality, and about when do we know it? Until the Piketty revolution swept through the field, most of what we knew about income and wealth inequality came from surveys, in which randomly chosen households are asked to fill in a questionnaire, and their answers are tallied up to produce a statistical portrait of the whole. The international gold standard for such surveys is the annual survey conducted once a year by the Census Bureau. The Federal Reserve also conducts a triennial survey of the distribution of wealth.

These two surveys are an essential guide to the changing shape of American society. Among other things, they have long pointed to a dramatic shift in the process of US economic growth, one that started around 1980. Before then, families at all levels saw their incomes grow more or less in tandem with the growth of the economy as a whole. After 1980, however, the lion’s share of gains went to the top end of the income distribution, with families in the bottom half lagging far behind.

Historically, other countries haven’t been equally good at keeping track of who gets what; but this situation has improved over time, in large part thanks to the efforts of the Luxembourg Income Study (with which I will soon be affiliated). And the growing availability of survey data that can be compared across nations has led to further important insights. In particular, we now know both that the United States has a much more unequal distribution of income than other advanced countries and that much of this difference in outcomes can be attributed directly to government action. European nations in general have highly unequal incomes from market activity, just like the United States, although possibly not to the same extent. But they do far more redistribution through taxes and transfers than America does, leading to much less inequality in disposable incomes.

Yet for all their usefulness, survey data have important limitations. They tend to undercount or miss entirely the income that accrues to the handful of individuals at the very top of the income scale. They also have limited historical depth. Even US survey data only take us to 1947.

Enter Piketty and his colleagues, who have turned to an entirely different source of information: tax records. This isn’t a new idea. Indeed, early analyses of income distribution relied on tax data because they had little else to go on. Piketty et al. have, however, found ways to merge tax data with other sources to produce information that crucially complements survey evidence. In particular, tax data tell us a great deal about the elite. And tax-based estimates can reach much further into the past: the United States has had an income tax since 1913, Britain since 1909. France, thanks to elaborate estate tax collection and record-keeping, has wealth data reaching back to the late eighteenth century.

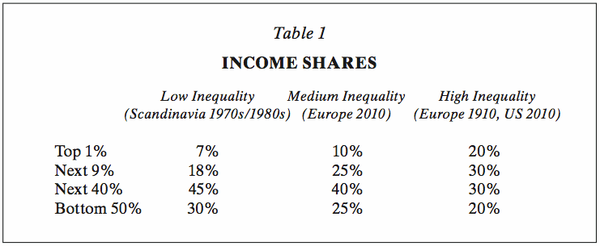

Exploiting these data isn’t simple. But by using all the tricks of the trade, plus some educated guesswork, Piketty is able to produce a summary of the fall and rise of extreme inequality over the course of the past century. It looks like Table 1 on this page.

As I said, describing our current era as a new Gilded Age or Belle Époque isn’t hyperbole; it’s the simple truth. But how did this happen?

2.

Piketty throws down the intellectual gauntlet right away, with his book’s very title: Capital in the Twenty-First Century. Are economists still allowed to talk like that?

It’s not just the obvious allusion to Marx that makes this title so startling. By invoking capital right from the beginning, Piketty breaks ranks with most modern discussions of inequality, and hearkens back to an older tradition.

The general presumption of most inequality researchers has been that earned income, usually salaries, is where all the action is, and that income from capital is neither important nor interesting. Piketty shows, however, that even today income from capital, not earnings, predominates at the top of the income distribution. He also shows that in the past—during Europe’s Belle Époque and, to a lesser extent, America’s Gilded Age—unequal ownership of assets, not unequal pay, was the prime driver of income disparities. And he argues that we’re on our way back to that kind of society. Nor is this casual speculation on his part. For all that Capital in the Twenty-First Century is a work of principled empiricism, it is very much driven by a theoretical frame that attempts to unify discussion of economic growth and the distribution of both income and wealth. Basically, Piketty sees economic history as the story of a race between capital accumulation and other factors driving growth, mainly population growth and technological progress.

To be sure, this is a race that can have no permanent victor: over the very long run, the stock of capital and total income must grow at roughly the same rate. But one side or the other can pull ahead for decades at a time. On the eve of World War I, Europe had accumulated capital worth six or seven times national income. Over the next four decades, however, a combination of physical destruction and the diversion of savings into war efforts cut that ratio in half. Capital accumulation resumed after World War II, but this was a period of spectacular economic growth—the Trente Glorieuses, or “Glorious Thirty” years; so the ratio of capital to income remained low. Since the 1970s, however, slowing growth has meant a rising capital ratio, so capital and wealth have been trending steadily back toward Belle Époque levels. And this accumulation of capital, says Piketty, will eventually recreate Belle Époque–style inequality unless opposed by progressive taxation.

Why? It’s all about r versus g—the rate of return on capital versus the rate of economic growth.

Just about all economic models tell us that if g falls—which it has since 1970, a decline that is likely to continue due to slower growth in the working-age population and slower technological progress—r will fall too. But Piketty asserts that r will fall less than g. This doesn’t have to be true. However, if it’s sufficiently easy to replace workers with machines—if, to use the technical jargon, the elasticity of substitution between capital and labor is greater than one—slow growth, and the resulting rise in the ratio of capital to income, will indeed widen the gap between r and g. And Piketty argues that this is what the historical record shows will happen.

If he’s right, one immediate consequence will be a redistribution of income away from labor and toward holders of capital. The conventional wisdom has long been that we needn’t worry about that happening, that the shares of capital and labor respectively in total income are highly stable over time. Over the very long run, however, this hasn’t been true. In Britain, for example, capital’s share of income—whether in the form of corporate profits, dividends, rents, or sales of property, for example—fell from around 40 percent before World War I to barely 20 percent circa 1970, and has since bounced roughly halfway back. The historical arc is less clear-cut in the United States, but here, too, there is a redistribution in favor of capital underway. Notably, corporate profits have soared since the financial crisis began, while wages—including the wages of the highly educated—have stagnated.

A rising share of capital, in turn, directly increases inequality, because ownership of capital is always much more unequally distributed than labor income. But the effects don’t stop there, because when the rate of return on capital greatly exceeds the rate of economic growth, “the past tends to devour the future”: society inexorably tends toward dominance by inherited wealth.

Consider how this worked in Belle Époque Europe. At the time, owners of capital could expect to earn 4–5 percent on their investments, with minimal taxation; meanwhile economic growth was only around one percent. So wealthy individuals could easily reinvest enough of their income to ensure that their wealth and hence their incomes were growing faster than the economy, reinforcing their economic dominance, even while skimming enough off to live lives of great luxury.

And what happened when these wealthy individuals died? They passed their wealth on—again, with minimal taxation—to their heirs. Money passed on to the next generation accounted for 20 to 25 percent of annual income; the great bulk of wealth, around 90 percent, was inherited rather than saved out of earned income. And this inherited wealth was concentrated in the hands of a very small minority: in 1910 the richest one percent controlled 60 percent of the wealth in France; in Britain, 70 percent.

No wonder, then, that nineteenth-century novelists were obsessed with inheritance. Piketty discusses at length the lecture that the scoundrel Vautrin gives to Rastignac in Balzac’s Père Goriot, whose gist is that a most successful career could not possibly deliver more than a fraction of the wealth Rastignac could acquire at a stroke by marrying a rich man’s daughter. And it turns out that Vautrin was right: being in the top one percent of nineteenth-century heirs and simply living off your inherited wealth gave you around two and a half times the standard of living you could achieve by clawing your way into the top one percent of paid workers.

You might be tempted to say that modern society is nothing like that. In fact, however, both capital income and inherited wealth, though less important than they were in the Belle Époque, are still powerful drivers of inequality—and their importance is growing. In France, Piketty shows, the inherited share of total wealth dropped sharply during the era of wars and postwar fast growth; circa 1970 it was less than 50 percent. But it’s now back up to 70 percent, and rising. Correspondingly, there has been a fall and then a rise in the importance of inheritance in conferring elite status: the living standard of the top one percent of heirs fell below that of the top one percent of earners between 1910 and 1950, but began rising again after 1970. It’s not all the way back to Rasti-gnac levels, but once again it’s generally more valuable to have the right parents (or to marry into having the right in-laws) than to have the right job.

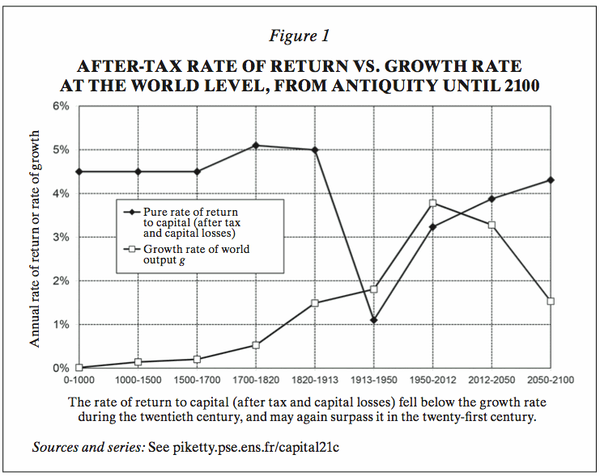

And this may only be the beginning. Figure 1 on this page shows Piketty’s estimates of global r and g over the long haul, suggesting that the era of equalization now lies behind us, and that the conditions are now ripe for the reestablishment of patrimonial capitalism.

Given this picture, why does inherited wealth play as small a part in today’s public discourse as it does? Piketty suggests that the very size of inherited fortunes in a way makes them invisible: “Wealth is so concentrated that a large segment of society is virtually unaware of its existence, so that some people imagine that it belongs to surreal or mysterious entities.” This is a very good point. But it’s surely not the whole explanation. For the fact is that the most conspicuous example of soaring inequality in today’s world—the rise of the very rich one percent in the Anglo-Saxon world, especially the United States—doesn’t have all that much to do with capital accumulation, at least so far. It has more to do with remarkably high compensation and incomes.

3.

Capital in the Twenty-First Century is, as I hope I’ve made clear, an awesome work. At a time when the concentration of wealth and income in the hands of a few has resurfaced as a central political issue, Piketty doesn’t just offer invaluable documentation of what is happening, with unmatched historical depth. He also offers what amounts to a unified field theory of inequality, one that integrates economic growth, the distribution of income between capital and labor, and the distribution of wealth and income among individuals into a single frame.

And yet there is one thing that slightly detracts from the achievement—a sort of intellectual sleight of hand, albeit one that doesn’t actually involve any deception or malfeasance on Piketty’s part. Still, here it is: the main reason there has been a hankering for a book like this is the rise, not just of the one percent, but specifically of the American one percent. Yet that rise, it turns out, has happened for reasons that lie beyond the scope of Piketty’s grand thesis.

Piketty is, of course, too good and too honest an economist to try to gloss over inconvenient facts. “US inequality in 2010,” he declares, “is quantitatively as extreme as in old Europe in the first decade of the twentieth century, but the structure of that inequality is rather clearly different.” Indeed, what we have seen in America and are starting to see elsewhere is something “radically new”—the rise of “supersalaries.”

Capital still matters; at the very highest reaches of society, income from capital still exceeds income from wages, salaries, and bonuses. Piketty estimates that the increased inequality of capital income accounts for about a third of the overall rise in US inequality. But wage income at the top has also surged. Real wages for most US workers have increased little if at all since the early 1970s, but wages for the top one percent of earners have risen 165 percent, and wages for the top 0.1 percent have risen 362 percent. If Rastignac were alive today, Vautrin might concede that he could in fact do as well by becoming a hedge fund manager as he could by marrying wealth.

What explains this dramatic rise in earnings inequality, with the lion’s share of the gains going to people at the very top? Some US economists suggest that it’s driven by changes in technology. In a famous 1981 paper titled “The Economics of Superstars,” the Chicago economist Sherwin Rosen argued that modern communications technology, by extending the reach of talented individuals, was creating winner-take-all markets in which a handful of exceptional individuals reap huge rewards, even if they’re only modestly better at what they do than far less well paid rivals.

Piketty is unconvinced. As he notes, conservative economists love to talk about the high pay of performers of one kind or another, such as movie and sports stars, as a way of suggesting that high incomes really are deserved. But such people actually make up only a tiny fraction of the earnings elite. What one finds instead is mainly executives of one sort or another—people whose performance is, in fact, quite hard to assess or give a monetary value to.

Who determines what a corporate CEO is worth? Well, there’s normally a compensation committee, appointed by the CEO himself. In effect, Piketty argues, high-level executives set their own pay, constrained by social norms rather than any sort of market discipline. And he attributes skyrocketing pay at the top to an erosion of these norms. In effect, he attributes soaring wage incomes at the top to social and political rather than strictly economic forces.

Now, to be fair, he then advances a possible economic analysis of changing norms, arguing that falling tax rates for the rich have in effect emboldened the earnings elite. When a top manager could expect to keep only a small fraction of the income he might get by flouting social norms and extracting a very large salary, he might have decided that the opprobrium wasn’t worth it. Cut his marginal tax rate drastically, and he may behave differently. And as more and more of the supersalaried flout the norms, the norms themselves will change.

There’s a lot to be said for this diagnosis, but it clearly lacks the rigor and universality of Piketty’s analysis of the distribution of and returns to wealth. Also, I don’t think Capital in the Twenty-First Century adequately answers the most telling criticism of the executive power hypothesis: the concentration of very high incomes in finance, where performance actually can, after a fashion, be evaluated. I didn’t mention hedge fund managers idly: such people are paid based on their ability to attract clients and achieve investment returns. You can question the social value of modern finance, but the Gordon Gekkos out there are clearly good at something, and their rise can’t be attributed solely to power relations, although I guess you could argue that willingness to engage in morally dubious wheeling and dealing, like willingness to flout pay norms, is encouraged by low marginal tax rates.

Overall, I’m more or less persuaded by Piketty’s explanation of the surge in wage inequality, though his failure to include deregulation is a significant disappointment. But as I said, his analysis here lacks the rigor of his capital analysis, not to mention its sheer, exhilarating intellectual elegance.

Yet we shouldn’t overreact to this. Even if the surge in US inequality to date has been driven mainly by wage income, capital has nonetheless been significant too. And in any case, the story looking forward is likely to be quite different. The current generation of the very rich in America may consist largely of executives rather than rentiers, people who live off accumulated capital, but these executives have heirs. And America two decades from now could be a rentier-dominated society even more unequal than Belle Époque Europe.

But this doesn’t have to happen.

4.

At times, Piketty almost seems to offer a deterministic view of history, in which everything flows from the rates of population growth and technological progress. In reality, however, Capital in the Twenty-First Century makes it clear that public policy can make an enormous difference, that even if the underlying economic conditions point toward extreme inequality, what Piketty calls “a drift toward oligarchy” can be halted and even reversed if the body politic so chooses.

The key point is that when we make the crucial comparison between the rate of return on wealth and the rate of economic growth, what matters is the after-tax return on wealth. So progressive taxation—in particular taxation of wealth and inheritance—can be a powerful force limiting inequality. Indeed, Piketty concludes his masterwork with a plea for just such a form of taxation. Unfortunately, the history covered in his own book does not encourage optimism.

It’s true that during much of the twentieth century strongly progressive taxation did indeed help reduce the concentration of income and wealth, and you might imagine that high taxation at the top is the natural political outcome when democracy confronts high inequality. Piketty, however, rejects this conclusion; the triumph of progressive taxation during the twentieth century, he contends, was “an ephemeral product of chaos.” Absent the wars and upheavals of Europe’s modern Thirty Years’ War, he suggests, nothing of the kind would have happened.

As evidence, he offers the example of France’s Third Republic. The Republic’s official ideology was highly egalitarian. Yet wealth and income were nearly as concentrated, economic privilege almost as dominated by inheritance, as they were in the aristocratic constitutional monarchy across the English Channel. And public policy did almost nothing to oppose the economic domination by rentiers: estate taxes, in particular, were almost laughably low.

Why didn’t the universally enfranchised citizens of France vote in politicians who would take on the rentier class? Well, then as now great wealth purchased great influence—not just over policies, but over public discourse. Upton Sinclair famously declared that “it is difficult to get a man to understand something when his salary depends on his not understanding it.” Piketty, looking at his own nation’s history, arrives at a similar observation: “The experience of France in the Belle Époque proves, if proof were needed, that no hypocrisy is too great when economic and financial elites are obliged to defend their interest.”

The same phenomenon is visible today. In fact, a curious aspect of the American scene is that the politics of inequality seem if anything to be running ahead of the reality. As we’ve seen, at this point the US economic elite owes its status mainly to wages rather than capital income. Nonetheless, conservative economic rhetoric already emphasizes and celebrates capital rather than labor—“job creators,” not workers.

In 2012 Eric Cantor, the House majority leader, chose to mark Labor Day—Labor Day!—with a tweet honoring business owners:

Today, we celebrate those who have taken a risk, worked hard, built a business and earned their own success.

Perhaps chastened by the reaction, he reportedly felt the need to remind his colleagues at a subsequent GOP retreat that most people don’t own their own businesses—but this in itself shows how thoroughly the party identifies itself with capital to the virtual exclusion of labor.

Nor is this orientation toward capital just rhetorical. Tax burdens on high-income Americans have fallen across the board since the 1970s, but the biggest reductions have come on capital income—including a sharp fall in corporate taxes, which indirectly benefits stockholders—and inheritance. Sometimes it seems as if a substantial part of our political class is actively working to restore Piketty’s patrimonial capitalism. And if you look at the sources of political donations, many of which come from wealthy families, this possibility is a lot less outlandish than it might seem.

Piketty ends Capital in the Twenty-First Century with a call to arms—a call, in particular, for wealth taxes, global if possible, to restrain the growing power of inherited wealth. It’s easy to be cynical about the prospects for anything of the kind. But surely Piketty’s masterly diagnosis of where we are and where we’re heading makes such a thing considerably more likely. So Capital in the Twenty-First Century is an extremely important book on all fronts. Piketty has transformed our economic discourse; we’ll never talk about wealth and inequality the same way we used to.

ZNetwork is funded solely through the generosity of its readers.

Donate